If you like this article then please like us on Facebook so that you can get our updates in future ……….and subscribe to our mailing list ” freely “

Meaning Fund Flow Statement

Funds flow statement is based on the concept of working capital while cash flow statement is based on cash which is only one of the element of working capital.

Fund means Working capital – difference between current assets and current liabilitiesFunds flow statement analyses the reasons for change in financial position between two balance sheetsFunds flow statement shows the inflows and outflows of funds – Sources and Application of funds during a particular period

Objective of Fund Flow Statement

Funds Flow Statement is a statement prepared to analyse the reasons for changes in the Financial Position of a Company between current year and previous financial year. It displays the inflow and outflow of funds.

How to prepare funds flow statements :

A.Working capital – changes :

For preparing the Funds Flow Statement, the first and foremost thing to be done is to prepare the Statement of Changes in Working Capital. There may be several reasons for changes in the Working Capital Position of any business concern. Some of the reasons are as follows. 1.Repayment of a Long Term loans or Redemption of Preference Shares without raising other long term resource. 2.Payments of amount towards Dividends in excess of the Profits earned. 3.Purchase of Fixed Assets or Long Term Investments without raising other types of long-term Long Funds.

B.Calculation of funds from operations:

Apart from investing an financing activities the company generates its major revenue from normal business operations. This is to be prepared by noting all the cash generating operations of the business.

Net Income

Add:

DepreciationAmortization of Intangibles and deferred chargesAmortization of loss on sale of investments or fixed assetsLosses from other non-operating itemsCurrent year tax provisionTransfer to reserveProposed dividend

Less:

Profit on sale of investment or fixed assetsAny subsidy credited to P & L A/cAny written back reserve and provision

C.Preparation of funds flow statement: While preparing the Funds Flow Statement, the Sources of funds and application of Funds are to be disclosed clearly so as to disclose the Sources from where the Funds have been generated the uses to which these Funds have been applied. This Statement is also sometimes referred to as the Sources and Applications of Funds Statement this is also called as Statement of Changes in Financial Position.

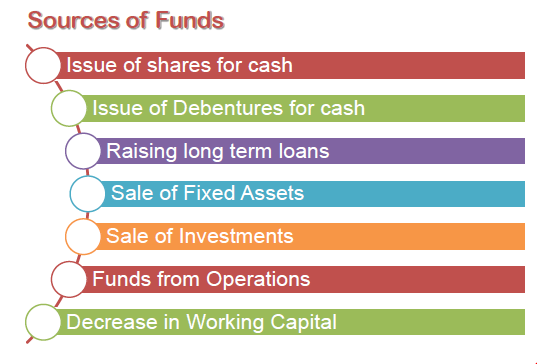

A. Sources of funds :

Funds can be procured from different sources available in the market Some of these are

Decline in working capital assetsFunds from OperationsSale of Investments and other Fixed AssetsIssue of Shares and Debentures for Cash.Long Term Loans.

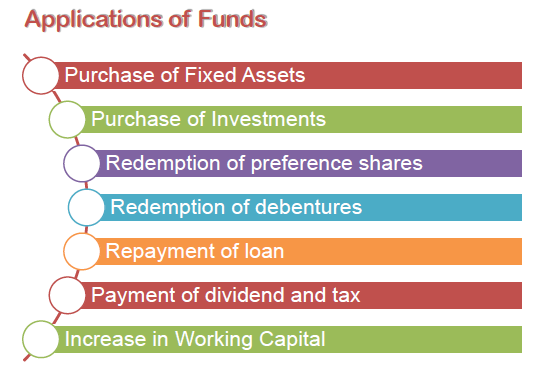

B. Applicatioon of funds :

Funds procured through different sources as stated above will be used in various applications as :

Increase in Working Capital.Redemption of Debentures, Preference Shares and Repayment of Loan.Payment of Dividend & Tax.Purchase of Fixed Assets.Purchase of investments.

Recommended Articles

Accrued Liabilities – Meaning, Definition with ExampleAccounting Entries for Service Tax, VAT and TDSAccounting Standard 15: Accounting for Retirement BenefitsList of Ind AS Notified by MCA – Indian Accounting StandardsAccounting for Rectification of ErrorsDistinguish Accounting, Auditing and InvestigationMeaning of Accounting & Scope of AccountingVarious Types of Vouchers In AccountingSubsidiary Books And Their Advantages